RSS Feed

RSS Feed

- 2026 | 7 Posts

- 2025 | 12 Posts

- 2024 | 12 Posts

- 2023 | 12 Posts

- 2022 | 13 Posts

- 2021 | 13 Posts

- 2020 | 12 Posts

- 2019 | 15 Posts

- 2018 | 15 Posts

Subscribe and receive email notifications of new blog posts.

3

How to Calculate Apartment Building Valuation in Northern Virginia; Gross Rent Multiplier - Return on Investment - Internal Rate of Return

What is Gross Rent Multiplier (GRM)?

In a recent blog post, I explained the use of Cap Rate by investors as a financial technique to estimate value when considering the buying or selling of a multi-family apartment building. Another metric used in real estate is Gross Rent Multiplier (GRM). Like Cap Rate, GRM is simply a gauge of value, but it can be used to quickly compare investment opportunities. GRM accounts for the gross rents as measured against the selling price. It's calculated by taking the price and dividing it by the total annual gross rent. For example, a price of $1 million divided by $100,000 in gross rent produces a GRM of 10. Generally, GRM's in the Northern Virginia region vary widely between 6 and 16 based upon building location, rent level, age, and class. Generally, the higher the GRM the better the building and lower the perceived risk. Likewise, the higher the GRM the longer it will take an investor to recover their investment, meaning a lower ROI.

GRM can be useful when quickly comparing investments, but it has a few inherent flaws. First, it calculates the gross rent with no adjustment for vacancy. No building goes 100% occupied at all times. Second, it does not at all take into consideration operating expenses and buildings can have very different expense profiles depending on management and building systems. Like Cap Rate, GRM is only a starting point in determining value. The only way to accurately determine enterprise valuation is by financially modeling the complete rent roll with vacancy, accounting for all expenses and loan costs, and calculating ROI & IRR like described in the next section.

Return on Investment (ROI) & Internal Rate of Return (IRR)

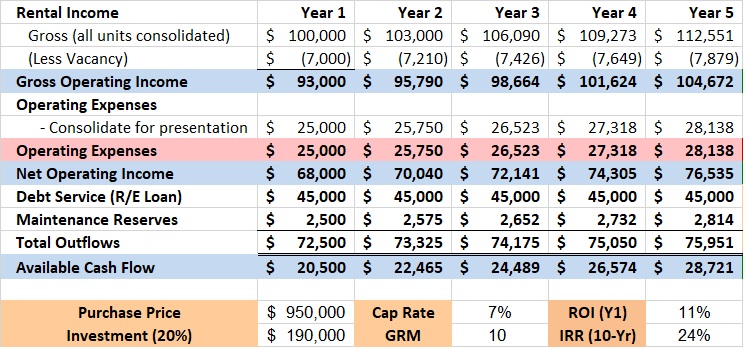

ROI and IRR are absolutely necessary when analyzing the buying or selling of an apartment building. Both methods require preparing a pro forma income statement like the table below. When in search of the most accurate investment performance, one must analyze all income against all expenses. This is the only way to evaluate the financial holy grail of any business - cash flow. Cash flow, and the resulting ROI and IRR calculations, are the tools of sophisticated investors, certified financial analysts, and lenders alike.

ROI Just Begins to Draw Back the Curtain

ROI is a popular metric because of its versatility and simplicity. It's important, because it requires preparing at least a Year 1 pro forma to estimate cash flow. This means consideration of the complete rent roll and vacancy, as well as accounting for all expenses, loan costs and even a maintenance reserve. The resulting free cash flow divided by the investment amount yields the investment profitability (ROI). However, ROI is very limited in that it only considers Year 1.

IRR Pulls Back the Financial Curtain Completely

Calculating the IRR should be the end game of any buyer or seller of an apartment building as it accounts for total return and long-term investment performance. As such, it requires preparing a multiple year income statement pro forma to forecast future rents and expenses. It requires contemplation of changes in loan costs, interest rates and when debt must be re-financed. It requires estimating capital improvements against the reserve fund, and even the net proceeds from a possible sale. The IRR is used to compare and contrast against the investor's hurdle rate. The hurdle rate is the minimum rate of return required by an investor to proceed with a project. The IRR must exceed, or jump over, the investor's minimum rate of return. Calculating the IRR is the only way to accurately measure investment performance, because it marries long-term projections with the long-term horizon under which a business actually operates.

The Calculations

⇒ Cap Rate = NOI / Purchase Price = $68,000/$950,000 = 7%

⇒ Building Value = NOI/Cap Rate = $68,000/0.07 = $950,000

⇒ GRM = Purchase Price/Total Gross Annual Rent = $950,000/$100,000 = 9.5

⇒ ROI = Investment/Cash Flow = $20,500/$190,000 = 11%

⇒ IRR = Time value of Investment + Cash Flow + Sale Proceeds = 24%

*IRR is the discount rate that makes the net present value of all cash flows equal to zero. It's calculated in a spreadsheet using a specific formula too detailed to fully describe here.

- 43777 Central Station Drive

- Suite 390

- Ashburn, VA 20147

Office: (571) 386-1075 Cell: (703) 568-6750 Email Me

Privacy Policy / DMCA Notice / ADA Accessibility