Tim Trainum Properties

"Delivering a Preferred Experience in Real Estate!"

REALTOR®, VA License #0225235004

Key Local Market Info!

RSS Feed

RSS Feed

RSS Feed

- 2026 | 7 Posts

- 2025 | 12 Posts

- 2024 | 12 Posts

- 2023 | 12 Posts

- 2022 | 13 Posts

- 2021 | 13 Posts

- 2020 | 12 Posts

- 2019 | 15 Posts

- 2018 | 15 Posts

Subscribe and receive email notifications of new blog posts.

April

8

8

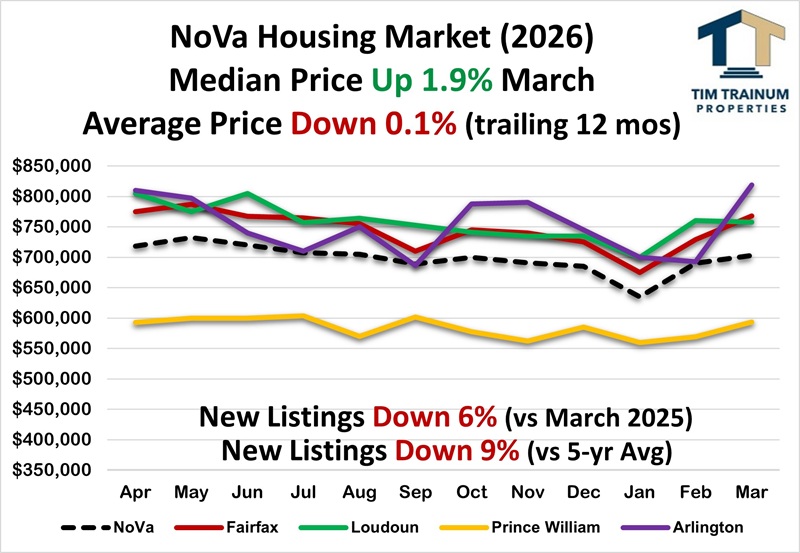

Northern Virginia Homes Selling Faster; Prices Flat, Weekly Listings at 2-Year Low

March Highlights:

- WEEKLY ACTIVE LISTINGS CONTINUE TO PLUMMET; PRICES FLAT

- Weekly Active Listings at 2-Year Low

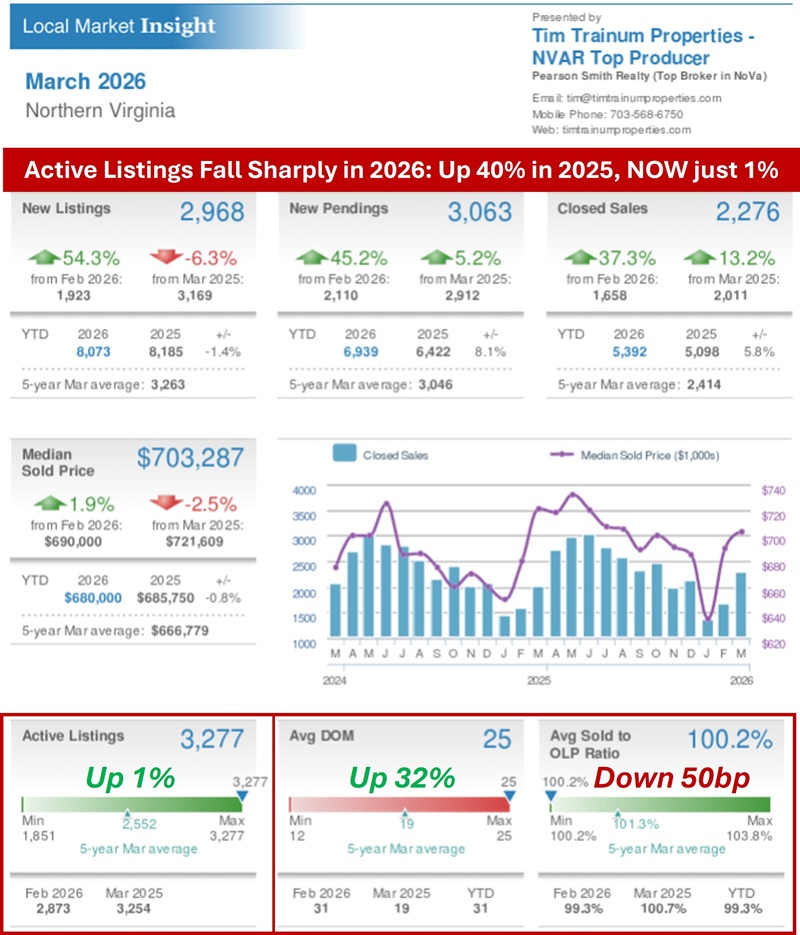

The movement of Weekly Active Listings is a good, secondary indicator of how supply and demand for homes are moving. During the five years before March 2024, the current number of Weekly Active Listings compared to the same week the year before was consistently lower underscoring excess demand and low inventory. Throughout 2024 and 2025, that measurement flipped with Weekly Active Listings higher than the year before, averaging 30 to 40% higher. This meant about 2,500 more homes in the D.C. metro area, pushing inventory higher as well as helping to balance the market between buyers and sellers. In 2026, this gap has declined week by week to its present 2-year low of just 1%, about 100 homes. Contrast this with New Listings from sellers (supply) which are generally flat through March (-1.4%). The result points to an uptick in buyer demand in recent months absorbing excess supply, and shifting the three important top-line market metrics toward sellers. Here is March 2026 compared to March 2025 - Active Listings (UP 1%), Days on Market (UP 32%), and Sold-to-List Price Ratio (DOWN 50bp). By comparison, Active Listings were UP 59% in March 2025 vs March 2024. - Buyer Showings UP 3% in March 2026

Buyer showings (demand) are up slightly in March 2026 over March 2025 (3%). However, this despite a significant decline in showings during parts of the winter when severe weather occurred. Despite the recent uptick in interest rates, March showings were still UP 2.8%. - Listings UP 54% from February to March

This bettered last March UP 49% as well as the typical average UP 43% during the last 6 years. March and April are seasonally the strongest months of the year for New Listings. - March Listings DOWN 9% vs. 5-year Average

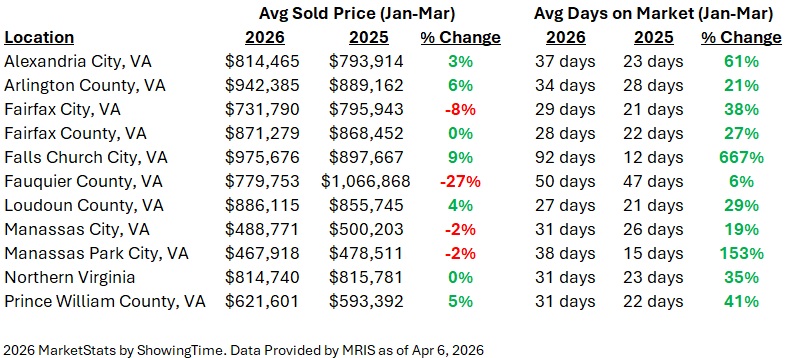

Seller listings stabilized in 2024, resisting the continued downtrend experienced in recent years. Listings remain down compared to long-term averages (-9%), but have substantially improved in Northern Virginia from down 20 to 40% in recent years. This improvement is primarily because the higher listing years before the pandemic continue to fall out of the 5-year calculation. March saw a significant increase in listings compared to last year (UP 13%). This new supply helped to increase total homes sold in Jan-Mar 2026 (5,392) compared to Jan-Mar 2025 (5,098) - UP 6%. - "Rate Locked Sellers" are UNLOCKING Increasing Inventory

In the wake of rising interest rates beginning in 2022, sellers largely "stayed in place" in 2023 and 2024. Sellers brought an increasing number of New Listings to the market in 2025 (UP 8%). This trend continued into 2026 with January listings UP 6% over Jan-2025. Thus far through March, New Listings are DOWN 1.4%, about 100 homes. The typical home seller is now 63 years old, a record high. This compares to age 54 in 2014 and age 45 in 2007. - Contract Ratio RISES to 0.97 (shift toward sellers)

Listings Under Contract represent 49% of the total March listings compared to those available and Active for sale at 51%. This is a further shift toward sellers from the 46/54 seen in February, and is running somewhat better than the 47/53 seen in March 2025. The shift toward sellers speaks to the marked drop in Weekly Active Listings previously mentioned in this report. Seller pricing remains relatively steady with Seller Price Reductions at 26% of currently Active listings. The importance of sellers correctly pricing a home in today's market cannot be overstated. - Inventory STEADY at DOWN 2% vs. March 2025

Inventory in Northern Virginia is steady in 2026 after 2025's fast-paced uptrend over 2024. March inventory of 1.37 months was almost equal to the 1.39 months in March 2025. Inventory has been held down with the rapid decline in Weekly Active Listings (currently just 1% higher - 100 listings in the DC Metro area). This presents a relatively more balanced buyer-seller market than experienced in 2020-24 when March inventory ranged from just 0.48 to 1.20 mos. - Sold-to-List Price Ratio DOWN with Rising Inventory

Buyer contract prices averaged 100.2% of Seller Asking in March. This is down from the 100.7% experienced in March 2025 and up from 99.3% last month. An improving Sold-to-List Price Ratio is typical in spring months with rising Contract Ratios. The contract cancellation rate has generally ranged between 12 and 18%. The current 12% is tracking more seller-advantaged than normal. - Speed to Contract is DOWN from 2025

Speed to contract improves for sellers, but continues its relatively slower pace with 60% of the 2,276 homes sold in March transacting in the fastest range (0 to 10 days). This is up significantly from 51% in February as seasonally experienced. By contrast, 24% of sales exceeded 30+ days on market, down from 35% last month. This is a moderate difference between now and last year. In March 2025, 66% of homes sold in the fastest range (0 to 10 days), while 60% in March 2026, down 6 points.

- Fed March Meeting: RATE STEADY at 3.50%

In line with market expectations, the Fed left its benchmark rate unchanged at the March meeting. Mortgage rates remained largely unchanged from Fed action as the bond market (which determines mortgage rates) was not anticipating a cut. The next meeting is scheduled for April 29. The futures market is presently pricing a 98% chance of no change in April. - Headline Inflation RISES to 3.3%, RISES to 0.9% Feb to Mar

Inflation spiked in March to 3.3% year-to-year compared to February (2.4%). Inflation month-to-month also spiked to 0.9% from February's 0.3%. Both numbers were in line with expectations given the recent rapid rise in energy prices. "Core Inflation" increased slightly to 2.6% from last month's 2.5%. Core inflation excludes more volatile energy and food prices. - Conventional Mortgage Rate RISES to Low 6's

With the recent stock market decline, mortgage rates increased with investor flight to safety. Rates increased about 1/2 point to 6.375% before trending down in recent days. Conforming rates are hovering around 6.125% and VA/FHA rates at 5.875%. Rates are still trading at a relative three-year low.

Tim Trainum Properties

Office: (571) 386-1075 Cell: (703) 568-6750 Email Me

- 43777 Central Station Drive

- Suite 390

- Ashburn, VA 20147

Office: (571) 386-1075 Cell: (703) 568-6750 Email Me

Privacy Policy / DMCA Notice / ADA Accessibility

This site is hosted, designed and copyright

© 1994 - 2026 by

Delta Media Group, Inc. -- Patent Pending --