Tim Trainum Properties

"Delivering a Preferred Experience in Real Estate!"

REALTOR®, VA License #0225235004

Key Local Market Info!

RSS Feed

RSS Feed

RSS Feed

- 2026 | 7 Posts

- 2025 | 12 Posts

- 2024 | 12 Posts

- 2023 | 12 Posts

- 2022 | 13 Posts

- 2021 | 13 Posts

- 2020 | 12 Posts

- 2019 | 15 Posts

- 2018 | 15 Posts

Subscribe and receive email notifications of new blog posts.

January

5

5

The Loan Amortization Schedule in Northern Virginia Has Completely Flipped to Buyer Benefit

Fall in Rates Flip Loan Amortization Schedule to Advantage Borrower

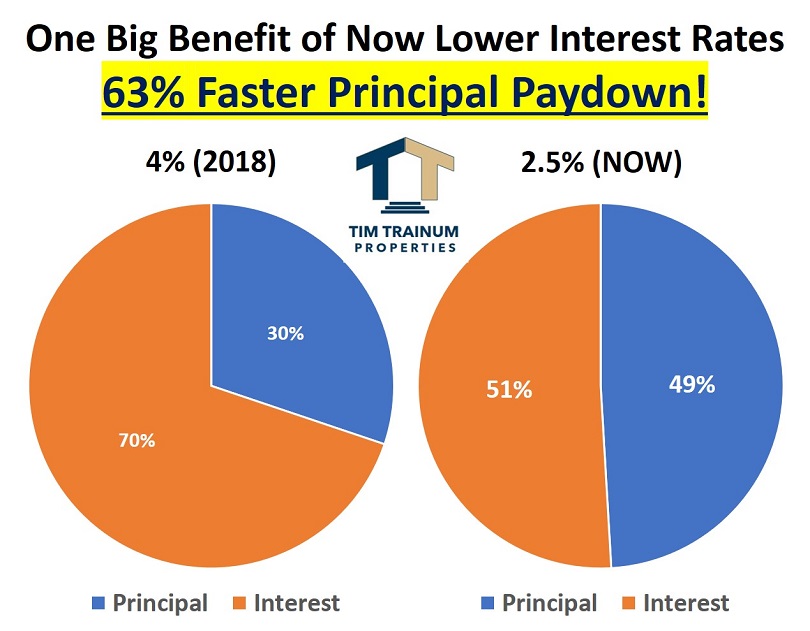

Just two years ago, interest rates for a home mortgage were in the area of 4%. Today, rates are near 2.5% (40% less). This 40% fall has dramatic, second-level benefits to borrowers beyond just a reduced mortgage payment and increased home purchasing power. Enter the Loan Amortization Schedule. Every month when a borrower makes a mortgage payment, part of the payment is applied toward interest and part toward principal. That amount changes little by little with every payment - more and more going toward principal and less toward interest. In 2018 when rates were 4%, the first mortgage payment on a loan was comprised of 70% interest and only 30% principal. Today, with rates near 2.5% this is now a 50/50 outcome and completely changes the velocity at which a borrower builds equity in their home. First-level thinkers know interest rates are at all-time lows, but second-level thinkers know exactly what that means in terms of the financial impacts that can seriously help clients make the most informed decisions.

Top 5 Things About Current Interest Rates & Amortization Schedule

- In 2018 at 4% interest, the first payment on a mortgage loan was comprised of a 70/30 split between interest/principal, but today's 2.5% rate produces a near 50/50 split at first payment.

- A borrower's loan paydown of principal (equity build-up) is occurring 63% faster now than it did two years ago.

- The borrower of a $500,000 30-year loan now pays $150,000 less interest over the life of the loan compared to 2018.

- At 4% interest, it takes 14 years of mortgage payments (168 payments) before the 70/30 interest-principal split works its way to 50/50. With today's rates, the tipping point dramatically reduces to just 10 payments.

- The "wealth accumulation effect" for homebuyers, investment property buyers (and re-finance borrowers) has improved considerably with far-reaching benefits to one's financial plan.

"My overarching objective is to be an advisor and value provider. I work to become the conduit of information to help consumers make the most informed decisions possible. I just happen to also have a real estate license." - Tim Trainum

Tim Trainum Properties

Office: (571) 386-1075 Cell: (703) 568-6750 Email Me

- 43777 Central Station Drive

- Suite 390

- Ashburn, VA 20147

Office: (571) 386-1075 Cell: (703) 568-6750 Email Me

Privacy Policy / DMCA Notice / ADA Accessibility

This site is hosted, designed and copyright

© 1994 - 2026 by

Delta Media Group, Inc. -- Patent Pending --